The markets are pretty much in an undecision pattern, Today's new high was quickly followed by a wave of selling that pushed prices lower by the end of the day.

I've decided to not touch any of my Iron Butterflies, I did take some of the contracts off the IBM Calendar.

Position's Details:

08/28 IBM Calendar

08/28 RUT Iron Butterfly

08/28 MNX Iron Butterfly

Friday, August 28, 2009

08/28 IBM Calendar

My gut feeling tells me IBM is heading lower. I took 2x 120 Calendars off the table for a slight profit and am getting myself ready to release them as 115 Calendars if needed. For now, that was all I needed to do to keep myself relaxed going through the weekend.

Previous Posting:

08/28 RUT Iron Butterfly

RUT started to show profits! That's nice! I tought about rolling the 650 CALL up, but decided against it. I'm not convinced the bulls are in total control yet. If we push higher I may give up Today's profit, but then I'll know where we are going. So far, we have been dancing around the 480 level and Today seemed we found a lot of selling once we traded at higher prices.

Previous Posting:

Previous Posting:

Previous Posting:

Previous Posting:08/28 MNX Iron Butterfly

Great P&L improvement Today, going through the weekend with a decent theta:delta ratio.

Previous Post:

Previous Post:

Previous Post:

Previous Post:Thursday, August 27, 2009

08/27 Daily Summary

I'm very happy to say I'm up just above 2% on the current open positions. Most positions did recover well after a few days of indecision in the market. As far as I'm concerned, let's stay directionless for another week, shall we?

I posted another KEY posting Today: When do I cut Deltas on Iron Butterflies? This is answering a question I have received a couple of times already: when/how do I cut deltas? I made my best to explain in there, everyone, feel free to share your thoughts, comments, etc.

Position's Details:

08/27 IBM Calendar

08/27 RUT Iron Butterfly

08/27 MNX Iron Butterfly

I posted another KEY posting Today: When do I cut Deltas on Iron Butterflies? This is answering a question I have received a couple of times already: when/how do I cut deltas? I made my best to explain in there, everyone, feel free to share your thoughts, comments, etc.

Position's Details:

08/27 IBM Calendar

08/27 RUT Iron Butterfly

08/27 MNX Iron Butterfly

When do I cut Deltas on Iron Butterflies?

I have seen this question a couple of times on the blog, and I must say, there is no exact answer, at least not from me. I don't have an exact formula, I go by a guideline and the most important thing for me is evaluating the trade every day before the market closes. One blog reader posted another blog where the author explains his formula, allow me to say a few things about how I have been doing it.

As I mentioned before, I have been following most of Dan Harvey's advice on how to trade these Iron Butterflies. Dan is a veteran trader who mentors at the Dan Sheridan program. I had the great pleasure of meeting him in San Francisco in one of Sheridan's seminars. Dan's rules are complex and quite well detailed, I follow most of them, but I'm the first to admit I'm still studying them, so can't claim to be a perfect follower. One of the most important things to know is that trading rules have to adapt to the trader's style, each trader has his/her own approach to things.

Also, important to notice is that the greeks will be quite different depending on the underlying you trade. The delta : theta ratio also depends on the size of the position, your willingness to take more or less risk, etc.

For the MNX position, I work in keeping the theta to delta ratio of 1:1, meaning if my theta is about 30, my delta shouldn't be much more than that. I also look at the risk profile and evaluate the 1-day 1-standard deviation move, if I notice that a 1-standard deviation move in any direction can take too much of my profits, I'll come in and cut some of the deltas. Every day I post those charts and the light-blue area is where Think or swim estimates 1 st. deviation to be for 1 day. Another rule-of-thumb I use is to place contingent orders in points where my delta is twice as much as my theta, to cut it in 1/2 and bring it back to a 1:1 ratio.. This has worked fairly well. I preffer to keep these contingent orders at least 1 standard deviation away from the closing price, otherwise it may whipsaw, as it happened to me back in June for my DIA Iron Butterfly trade.

For the RUT position, I don't know yet.. Sorry, no genius here, just a guy working on his craft :) I believe Dan Harvey recommends a theta to delta ratio of 3:1. However, this is for larger positions, My RUT position is the same size of the MNX, and because this is the first time I trade it, I'm not quite sure where the ratio should be. Honestly, I've been looking at the 1-day 1-st. deviation zone in the profile chart and evaluating if I can handle that kind of move, if not, I cut the deltas, if yes, I simply place the contingent orders there.

I try cutting the deltas in about 1/2 when I use contingent orders. It is BEST when you do this overnight and stop looking at it. This very month, I was watching when the MNX dropped 2 st. deviations and I over-adjusted the trade. The best practice, as far as I can tell from back-testing is to cut it in 1/2 and cut in 1/2 again if it keeps on moving.

Then again, evaluating the position at the end of the day is the most critical element here. I ask myself the question: If we go Up, am I ok? If we go Down, am I ok? If not, I adjust before closing, if yes, I put contingent orders around the 1 st. deviation zone.

I hope this helps, feel free to post your comments, share ideas, suggestions.. It is an open board here.

Cheers to our Success!

Gustavo

First the other trader's opinion is here:

http://www.optionsropeadope.com/2008/05/13/greek-exposure-calculations/

As I mentioned before, I have been following most of Dan Harvey's advice on how to trade these Iron Butterflies. Dan is a veteran trader who mentors at the Dan Sheridan program. I had the great pleasure of meeting him in San Francisco in one of Sheridan's seminars. Dan's rules are complex and quite well detailed, I follow most of them, but I'm the first to admit I'm still studying them, so can't claim to be a perfect follower. One of the most important things to know is that trading rules have to adapt to the trader's style, each trader has his/her own approach to things.

Also, important to notice is that the greeks will be quite different depending on the underlying you trade. The delta : theta ratio also depends on the size of the position, your willingness to take more or less risk, etc.

For the MNX position, I work in keeping the theta to delta ratio of 1:1, meaning if my theta is about 30, my delta shouldn't be much more than that. I also look at the risk profile and evaluate the 1-day 1-standard deviation move, if I notice that a 1-standard deviation move in any direction can take too much of my profits, I'll come in and cut some of the deltas. Every day I post those charts and the light-blue area is where Think or swim estimates 1 st. deviation to be for 1 day. Another rule-of-thumb I use is to place contingent orders in points where my delta is twice as much as my theta, to cut it in 1/2 and bring it back to a 1:1 ratio.. This has worked fairly well. I preffer to keep these contingent orders at least 1 standard deviation away from the closing price, otherwise it may whipsaw, as it happened to me back in June for my DIA Iron Butterfly trade.

For the RUT position, I don't know yet.. Sorry, no genius here, just a guy working on his craft :) I believe Dan Harvey recommends a theta to delta ratio of 3:1. However, this is for larger positions, My RUT position is the same size of the MNX, and because this is the first time I trade it, I'm not quite sure where the ratio should be. Honestly, I've been looking at the 1-day 1-st. deviation zone in the profile chart and evaluating if I can handle that kind of move, if not, I cut the deltas, if yes, I simply place the contingent orders there.

I try cutting the deltas in about 1/2 when I use contingent orders. It is BEST when you do this overnight and stop looking at it. This very month, I was watching when the MNX dropped 2 st. deviations and I over-adjusted the trade. The best practice, as far as I can tell from back-testing is to cut it in 1/2 and cut in 1/2 again if it keeps on moving.

Then again, evaluating the position at the end of the day is the most critical element here. I ask myself the question: If we go Up, am I ok? If we go Down, am I ok? If not, I adjust before closing, if yes, I put contingent orders around the 1 st. deviation zone.

I hope this helps, feel free to post your comments, share ideas, suggestions.. It is an open board here.

Cheers to our Success!

Gustavo

First the other trader's opinion is here:

http://www.optionsropeadope.com/2008/05/13/greek-exposure-calculations/

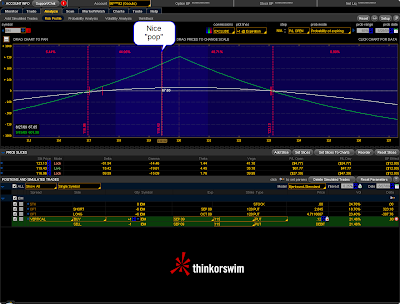

08/27 IBM Calendar

Today we had a nice "pop" in profits, if we get to 10% in about a week, You can look for me running for the exit, otherwise I'll stay for the full 15% ROI.

Previous Posting:

Subscribe to:

Posts (Atom)